- Pivot & Flow

- Posts

- War and Stagflation

In partnership with

Happy Sunday.

I'm going to skip the war recap. You know the news.

You know what's happening with Iran. This letter is about what actually changed for money this week, and I think it's bigger than most people realize.

The one sentence version: stagflation showed up in the data on Friday, and every traditional hedge failed at the same time.

Stagflation is no longer a debate

Friday's jobs report is the most important print we've gotten in months. The economy lost 92,000 jobs. Not "added fewer than expected." Lost them. Nobody on Wall Street had a negative number in their model. Manufacturing, healthcare, leisure, construction, all negative. The Kaiser strike explains part of the healthcare miss, but the weakness was broad. This is the fifth month of job losses in the last nine.

Wages came in at 0.4% month over month. Hot. A labor market cracking while the cost of employing people keeps rising. That's the definition of stagflation. It's sitting in the BLS data now, not just on Twitter.

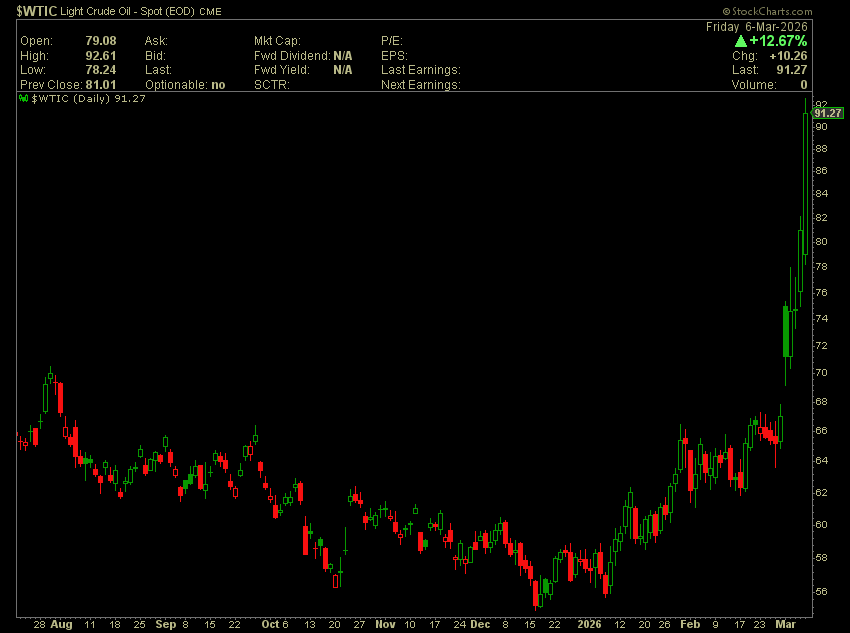

Layer oil on top. Crude closed at $90.90 Friday. The biggest weekly gain in the history of oil futures. Not the biggest in a year. The biggest ever. Trump posted that there will be no deal without Iran's unconditional surrender. That is not language that brings oil down.

The Atlanta Fed's GDPNow tracker dropped from 3.0 to 2.1 in a single week. Chicago Fed's Goolsbee said the word stagflation on live television. When a sitting Fed official uses that word, it's because they've already run the scenarios internally.

A week ago the market was pricing three rate cuts in 2026. Today it's pricing zero. In five trading days, the entire rate path got wiped out. That reprices housing, growth stocks, bank margins, commercial real estate, all of it.

The hedges are breaking

This is the part getting under-discussed.

Tuesday, Iran officially shut the Strait. Markets panicked. But nobody bought gold. They dumped it. Gold fell 4%. Silver dropped 8%. The precious metals trade, the one that's supposed to protect capital in a geopolitical crisis, didn't work.

What did work? The US dollar. Investors went straight to cash. That tells me something specific: this wasn't inflation hedging. It was a pure liquidity grab. People wanted the one asset they can always sell. That's a fear signal, not a positioning signal.

Wednesday, bonds sold off with stocks. That's not supposed to happen. In a normal crisis, money flows into treasuries and yields fall. Instead, yields climbed because the market started pricing energy-driven inflation over safety. The 60/40 portfolio failed.

Friday it got worse. BlackRock gated its flagship private credit fund. Investors asked to pull more than double the quarterly cap. When BlackRock tells investors "sorry, you can't have your money back," that's a flashing light. Blackstone's flagship fund saw $1.7 billion in net outflows the same week. Private credit has been the most crowded trade in fixed income for two years. If a third major fund gates, we have a liquidity problem that goes beyond war premium pricing.

Treasuries, gold, and private credit all failed in the same week. An energy shock with sticky inflation breaks the traditional playbook.

The only things that worked were US dollars and energy stocks.

Two markets, one tape

The market stopped trading as one group this week and broke into two: companies that benefit from or survive an energy shock, and everything else.

Energy was the only green sector. XLE held while every other sector ETF finished red. Defense names ran hard after Trump escalated. Lockheed, Northrop, and RTX all caught aggressive bids. Costco beat and held up because warehouse spending stays sticky even when gas prices spike.

Software caught a bid Thursday and Friday but I wouldn't read too much into it. Salesforce, Intuit, Okta, these names got destroyed over the prior three weeks. This looked more like a technical bounce off oversold levels than any kind of structural rotation.

The AI infrastructure names are a different story. Marvell jumped 18% after earnings. Management guided revenue growth accelerating every quarter. Broadcom's AI revenue doubled and they guided Q2 above the Street by $1.5 billion. Those capex budgets were committed 12 to 18 months ago. They're not getting pulled because crude is at $90. AI chip demand is running its own cycle, disconnected from the broader macro picture.

Then there's Berkshire. Greg Abel restarted buybacks for the first time since mid-2024 and put $15 million of his own money into the stock. He consulted directly with Buffett on intrinsic value and timing. When the guy running a $1 trillion conglomerate with $373 billion in cash starts spending his own paycheck on shares, that's worth noting.

On the other side, regional banks got destroyed. Western Alliance fell 8.46% and every single stock in the KBE bank ETF finished red. The 2-10 spread widened to 57 basis points. Wider spread normally helps banks, but not when it's widening because inflation expectations are blowing out while the short end stays anchored by a Fed that can't cut. That's margin compression with credit risk attached.

Airlines are in rough shape. United's CEO warned fuel costs are taking a real bite out of first-quarter results. Delta and Southwest fell in sympathy. Every dollar oil goes up hits their margins immediately. Cruise lines same deal. Norwegian extended losses all week.

The momentum trades unwound completely. Small caps, international markets, memory chips, the broadening thesis that was working for months died the second this conflict escalated. South Korea's market lost 18% in two days. Worst drawdown since 1985. Samsung and SK Hynix are half the index and their factories run on imported Middle East energy.

The pattern is clear enough. The market is telling you what it's afraid of and what it isn't. Energy shock survivors held. Rate-cut-dependent names didn't. Names with fuel as a major input cost got punished immediately. That's the lens the tape is using right now, and it won't change until either oil comes down or the Fed finds a reason to move.

Today’s Sponsor

The $4 Billion Problem Hiding in Nearly Every Fast-Food Location

You show up to your favorite fast-food restaurant for a quick meal. But the line is too long, and you’re starving. So you bail.

You’re not alone. 93% of monthly fast-food visitors in America say their top frustration is long lines. And while you miss out on chicken nuggets and fries, restaurant owners lose significant revenue they can’t afford to miss.

So brands like White Castle use Miso Robotics’ AI-powered kitchen restaurant robots to run their fry stations, keeping kitchen operations smooth, workers safe, and customers happy.

Aided by a collaboration with NVIDIA, Miso’s AI-powered Flippy Fry Station robot works 2X faster than average fry cooks. That means operators serve more customers and unlock up to 3X more profits per location. And that means much shorter lines for you.

This is a paid advertisement for Miso Robotics’ Regulation A offering. Please read the offering circular at invest.misorobotics.com.

What I'm watching

CPI next week.

This lands in a completely different context now. If core CPI comes in above expectations, rate cuts are dead for all of 2026. Any upside surprise with oil at $90 locks the Fed in place. A downside surprise probably doesn't matter because energy hasn't fully flowed through yet. Watch the 2-year yield reaction more than the equity tape. If the 2-year doesn't fall on a cool print, the bond market is telling you it doesn't believe it.

Strait of Hormuz tanker traffic.

Forget what Iran says. Forget what Bessent promises. Watch what ships do. The Navy escort plan sounds good on paper, but analysts say Iran can harass that waterway with drones for months. If AIS tracking data shows tankers resuming transit, oil pulls back toward $80 and the war premium fades. If traffic stays paused, $100 oil becomes the base case.

Light Crude this week

Private credit fund flows.

BlackRock gated. Blackstone bled. If a third major fund announces gates or elevated redemption requests, we have a systemic liquidity problem forming in private credit. That spills into public markets fast because these funds hold levered positions that need to be unwound. Blue Owl already got downgraded this week.

The helium squeeze.

Qatar's shutdown cut off a third of the world's helium supply. Chipmakers need helium for semiconductor manufacturing. All three of Qatar's production facilities are offline. If repairs take more than two weeks, tech hardware supply chains face real bottlenecks. Small problem that gets big fast.

That's the week. Stagflation went from a debate to data. The traditional hedges failed. And the market split into two groups: energy shock survivors and everything else.

I don't know how long this lasts. Nobody does. But the rate cut cavalry isn't coming, oil has no policy fix, and private credit is starting to crack.

See you Monday.

Today’s Sponsor

That's when I'm predicting Elon Musk will announce the SpaceX IPO... in what Bloomberg is calling "the biggest listing of ALL TIME."

And I've found a 'backdoor' way to grab a Pre-IPO stake... BEFORE Elon makes the big announcement!

At a $1.5 TRILLION valuation... that would be 3,000 times bigger than Amazon's IPO.

This is a "millionaire-maker" event...